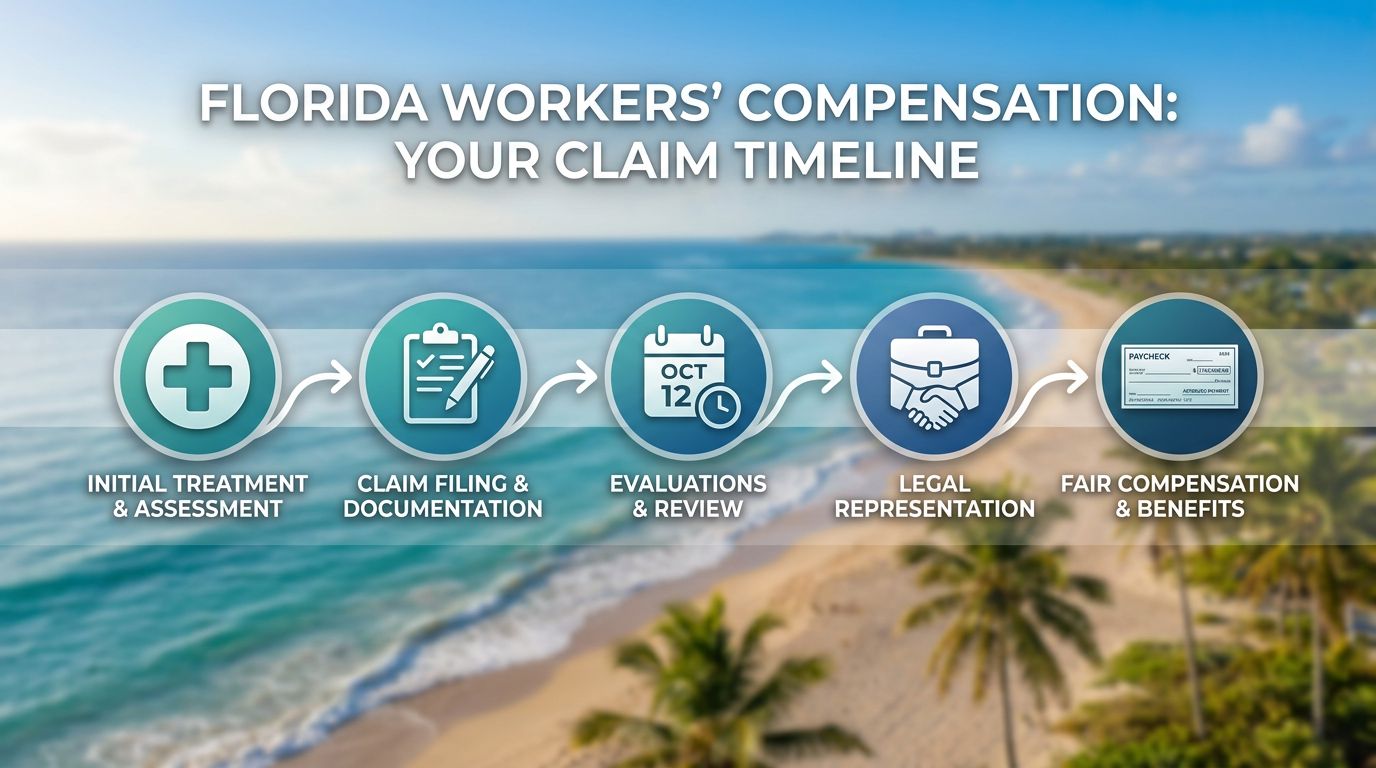

Florida Workers’ Comp Timeline From Injury Report To First Check

Getting hurt at work can feel like someone hit pause on your whole life. You’re in pain, you’re missing hours, and bills don’t wait.

The Florida workers comp timeline is built around deadlines and paperwork. When you know the order of events, it’s easier to spot delays and protect your benefits. Below is what usually happens from the moment you report the injury to the time your first wage-loss check should arrive.

Day 0 to Day 2: Report the injury, get treated, and lock in the details

First, get medical help. If it’s an emergency, go to the ER or call 911. After that, notify your supervisor as soon as you can, even if the injury seems minor.

Florida gives most workers up to 30 days to report a work injury to the employer, but waiting is risky. The state’s guidance is clear: report it as soon as possible, or a carrier may dispute the claim later. The Florida Division of Workers’ Compensation explains this deadline in its injured worker FAQs and its how to report an injury guide.

While the facts are fresh, write down the basics:

- When and where it happened

- What you were doing right before it happened

- Names of witnesses

- Photos of the area or equipment (if you can do it safely)

Also, ask who the insurance carrier is and where you should go for authorized care. In Florida, the carrier usually controls medical treatment, so going to your own doctor without approval can create headaches.

If you want a practical checklist for the first 24 hours, see Avard Law’s guide on steps after a workplace injury in Florida.

Days 3 to 10: Employer notice to the insurer and the claim “opens”

Once your employer knows about the injury, the next clock starts. Florida’s workers’ comp guidance says the employer should report the injury to the insurance carrier as soon as possible, but no later than 7 days after knowledge. That same FAQ also notes the carrier must send you an informational brochure within 3 days after it receives notice from the employer. You can confirm those benchmarks in the injured worker FAQs.

During this stage, a few things typically happen quickly:

An adjuster gets assigned. You may receive a claim number and instructions for medical care.

The carrier schedules an authorized doctor. If you already treated somewhere, the carrier may request records.

Wage information gets requested. The insurer needs your average weekly wage to calculate checks, so missing payroll details can slow payment.

Keep your communication tight and consistent. If the adjuster calls, take notes. If you send documents, save a copy. Think of it like building a receipt trail. Small gaps often become big disputes later.

For a broader look at how Florida’s system moves a claim from report to benefits, the state provides a benefit delivery process overview.

Days 11 to 21: Work status matters, because wage checks don’t start for everyone

Many people expect workers’ comp to pay them the minute they report an injury. In reality, medical care can start before wage checks do, and some claims never involve wage-loss payments at all.

Your first check depends on two things:

- Your doctor’s work status (taken completely off work, or placed on restrictions)

- Whether you actually lose wages because of that status

If the authorized doctor says you can do full duty, you might have medical coverage but no indemnity check. On the other hand, if the doctor takes you out of work, wage-loss benefits may apply.

A common surprise in Florida is the waiting period. Even when wage benefits apply, the first week can work differently than people expect.

Florida generally has a 7-day waiting period before disability wage benefits begin, and that waiting week may become payable if the disability lasts long enough. The state explains benefit basics and timelines in its workers’ compensation system guide (PDF).

Here’s a quick timeline snapshot to keep the steps straight:

| Timeframe | What usually happens | Who acts | What you should do |

|---|---|---|---|

| Same day to 2 days | Injury, first treatment, initial report | You | Report immediately, document what happened |

| Up to 30 days | Legal deadline to report to employer | You | Don’t wait, late notice can threaten the claim |

| Up to 7 days after employer knows | Employer reports to carrier | Employer | Ask for carrier name, claim number, adjuster contact |

| Within 3 days after carrier gets notice | Brochure explaining rights and duties | Carrier | Read it, it outlines required steps |

| Week 2 to 3 | Work status reports drive wage-loss eligibility | Authorized doctor, carrier | Attend appointments, follow restrictions |

The takeaway is simple: the “first check” clock often starts when the carrier has notice, the doctor documents disability, and the waiting period rules are met.

When should the first workers’ comp check arrive in Florida?

If your doctor takes you out of work and the carrier accepts the wage-loss portion of the claim, the first check often arrives within a few weeks, not a few days. Delays usually trace back to missing wage records, unclear work restrictions, or disputes about how the injury happened.

Also, workers’ comp checks are typically paid on a regular schedule after benefits start, often every two weeks. Your first payment may cover only the payable period under Florida’s waiting period rules, then the schedule settles into a rhythm.

If payments come late when they’re owed, Florida law can allow penalties and interest in certain situations. The details depend on the type of benefit and the facts of the delay, so it’s worth documenting every missed date and every explanation you’re given.

If your first check doesn’t show up: the most common reasons and what to do next

When a first check doesn’t arrive, it’s tempting to assume the insurer is ignoring you. Sometimes it’s simpler than that, but you still need to act.

Common causes include:

Late injury reporting: Waiting weeks to report gives the carrier room to argue the injury happened elsewhere.

Unauthorized treatment: If the carrier didn’t authorize the doctor, it can trigger disputes about work status and disability notes.

No written “out of work” status: If the doctor doesn’t clearly take you off work, wage benefits can stall.

Employer disputes: The employer may claim you weren’t working, or that you violated safety rules.

If you suspect a denial or disqualification issue, review these common pitfalls: reasons for workers’ comp denial in Florida.

As a practical next step, ask the adjuster in writing: (1) whether indemnity benefits were accepted or denied, (2) the benefit start date they used, and (3) what documents they still need. Then keep copies.

If you need the state’s roadmap for disputes, forms, and the benefit process, start with the Florida Division of Workers’ Compensation resources.

Bottom line: a clear timeline helps you catch problems early

The fastest workers’ comp claims usually have three things in common: prompt reporting, authorized medical care, and clean work status notes. Once one of those breaks, the first check often gets pushed back.

If something feels off, don’t wait for the problem to fix itself. Getting advice early can protect your benefits and reduce the chance of a drawn-out dispute.